The Consumer Financial Protection Bureau has filed a lawsuit against Capital One, alleging that the bank misled customers regarding its savings accounts. The lawsuit, initiated in mid-January 2025, claims that Capital One created confusion by promoting a high-yield savings account while allowing a lower-yield account to remain stagnant, impacting customers’ potential earnings.

- Median American household savings: $10,000

- High-yield savings accounts offer 4% interest

- Average savings account interest rate: 0.4%

- Major banks provide minimal interest rates

- Capital One accused of misleading customers

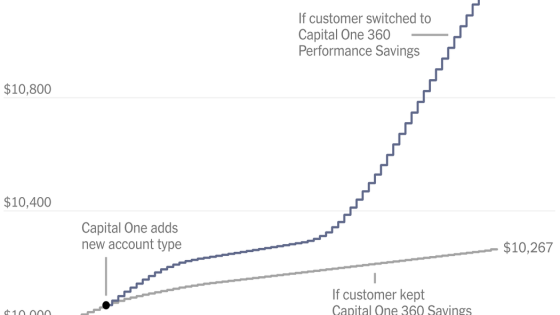

- CFPB estimates $2 billion avoided payments

The issue arises from the disparity in interest rates offered by banks. The median American household has about $10,000 in checking and savings accounts, with high-yield accounts providing nearly 4 percent annual interest, translating to approximately $400 yearly. In contrast, the average savings account interest rate is around 0.4 percent, with major banks like Bank of America, Chase, and Wells Fargo offering as low as 0.01 percent, resulting in just $1 in interest per year for a $10,000 deposit.

Capital One’s actions, as outlined by the Consumer Financial Protection Bureau, involved promoting its 360 Performance Savings account while neglecting the existing 360 Savings account, which offered lower interest rates. This strategy reportedly led to an estimated $2 billion in avoided payments to customers who were not informed about the benefits of switching accounts.

Many consumers may not actively seek better savings options, often due to inertia or a lack of awareness. Banks capitalize on this tendency by providing convenient services like numerous branches and ATMs, which can deter customers from exploring higher-yield alternatives. The lawsuit highlights the importance of transparency in banking and the need for consumers to be informed about their options.

This lawsuit underscores the critical need for consumers to understand their banking options and for banks to maintain transparency in their offerings. As interest rates remain low, awareness of potential earnings from high-yield accounts can significantly impact consumers’ financial health.